A Bi-Monthly Analysis of UHNW Asset Liquidity

Key Trends in UHNW Asset Liquidity

Standard market indicators (which typically measure sector specific transaction value, volume, and pricing) often fail to directly capture the unique and nuanced pressures affecting illiquid assets that high-net-worth individuals and families hold in their portfolios.

To address this gap and provide a clearer view of liquidity across unique assets, we developed the Leyster Liquidity Strength Index, a proprietary framework that incorporates factors such as shifting tastes, embedded leverage by asset type, and the market breadth of qualified buyers and sellers – each of these factors have significant, but varying, impacts on the overall liquidity scores we assign through our analysis.

The Leyster Liquidity Lens is our bi-monthly analysis powered by this index. It provides advisors and their clients with a consistent, data-driven view on the ease (or difficulty) with which private and alternative assets can be converted to cash. UHNW investors typically hold multiple illiquid positions, making it crucial to distinguish which can be mobilized quickly and which cannot.

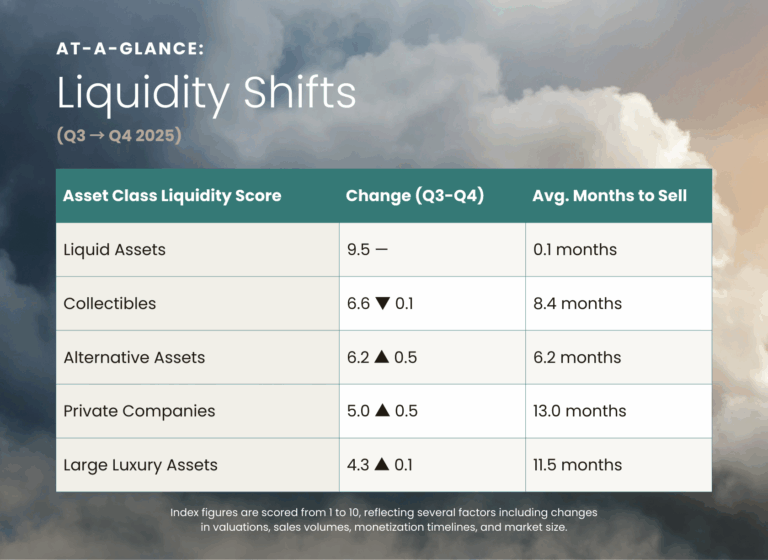

Comments on changes from October 2025 to December 2025:

Collectibles:

While headline conditions appear largely unchanged, the past two months mark a quiet but meaningful inflection in collectible asset liquidity. Aggregate valuations have inched higher, driven almost entirely by UHNW demand for the rarest, highest-quality pieces.

In autos, the upper tier blue-chip classics continue to hold value, whereas second-tier classics are experiencing pronounced declines. However, many potential buyers at all levels remain on the sidelines, waiting for clearer economic signals before re engaging with the auction market. Mecum’s Kissimee auction in Janaury will serve as a leading indicator for the broader collector car market.

The art market, most visibly demonstrated during New York’s fall auction week, reflects this bifurcation even more starkly. The three major auction houses generated roughly $2.2 billion in sales over the week, up more than 70% YOY, anchored by the $236 million sale of Gustav Klimt portrait, a record for Sotheby’s. Notably, buyers who spent much of the past year inactive returned, but focused almost exclusively on best-in-class works.

Watches and wine saw modest upticks as well, suggesting a tentative but growing sense of optimism across the broader collectibles landscape.

Alternative Assets:

Continued improvements in liquidity within the alternative asset segment are largely driven by an influx of dry powder across both existing and newly formed secondaries and royalty focused funds. In commercial real estate, vacancy rates are beginning to ease slightly, potentially signaling a market trough – though gains remain geographically split and concentrated in high-quality assets.

Large Luxury Assets:

The pattern emerging in collectibles is increasingly visible across large luxury assets as well. The resilience in this segment is being carried disproportionately by UHNW Americans, who now account for a growing share of demand for the highest-end yachts, homes, and private aircraft.

Top-line transaction activity in UHNW residential real estate remains positive, but value is concentrating further in select “destination suburb” markets (Palm Beach, Greenwich/Connecticut enclaves, and similar pockets) while pricing across major metros has remained largely unchanged or slightly decreased. Notably, sellers who were unwilling to negotiate during the pandemic-era boom are now accepting modest discounts access liquidity.

Meanwhile, underlying indicators in private aviation and yachting remain broadly in line with prior years, underscoring a market that is steady but increasingly dependent on a narrow band of UHNW buyers.

Leyster Takeaway

Excluding major market outliers (media mega deals, prominent asset sales, etc.), December activity has been uncharacteristically subdued for the typical UHNW family. For those who own premier best in class assets, liquidity is at an all time high. However, for most other assets, UHNWIs need to conduct an honest valuation reset. Continuing to anchor to pandemic era peaks and waiting for price surge/recovery is no longer viable. Prolonged indecision in today’s bifurcated market is a direct tax on future liquidity.

DISCLOSURE:

METHODOLOGY

Leyster Capital’s Liquidity Strength Index is a proprietary framework designed to assess the relative ease with which ultra-high net worth (UHNW) assets can be converted to cash—without sacrificing control or value. Each asset category is assigned a score reflecting its liquidity profile based on real-time market behavior, financing accessibility, and buyer dynamics.

- Low Liquidity Scores indicate assets with constrained buyer pools, elongated sale timelines, and limited financing options. These are typically one-of-a-kind or highly specialized holdings, such as large superyachts or highly bespoke real estate.

- Moderate Liquidity Scores reflect stable-to-growing asset classes with active buyer markets, evolving valuations, and expanding capital solutions. Collector cars and high-value watches often fall within this range.

- High Liquidity Scores are reserved for asset classes that benefit from deep capital markets, short transaction cycles, and consistent financing access, such as publicly traded securities and select commodities.

Leyster’s metrics are derived from quarterly or semi-annual data across a curated basket of assets, each weighted proportionally to its market size within its segment. Categories include:

- Large Luxury Assets: Ultra-luxury homes, private aircraft, and large yachts.

- Alternative Assets: LP/GP interests in private equity and private credit funds, income-producing commercial real estate, and entertainment royalties.

- Collectibles: Blue-chip collector cars, fine art, rare timepieces, and investment-grade wine.

All liquidity assessments are based on publicly available data from trusted sources including S&P, Pitchbook, Bloomberg, Evercore, UBS Art Basel, Knight Frank, and Cushman & Wakefield.

The assessments are supplemented by publicly available data from reputable sources within niche asset classes including Hagerty, International Federation of the Phonographic Industry, BoatPro, Global Jet Capital, ArtPrice, and Liv-ex. Assessments are further validated by conversations with UHNW asset owners, relevant financing providers, and key advisors.

This methodology underpins Leyster’s ongoing commentary and charting of liquidity stress indicators across UHNW portfolios. It remains consistent across reporting periods and serves as a foundational benchmark in our analysis.